The Covid-19 pandemic has been an unprecedented event that affected the lives of people all over the world. We have seen the impact it has had on businesses, particularly small to medium enterprises, and how it has forced them to make difficult decisions such as retrenchment. This has placed many people in a dire financial situation, often leading them to consider dipping into their retirement funds, the largest source of savings for most South Africans, to make ends meet.

The National Treasury took note of this and in 2021 proposed to make changes to the retirement fund system and introduce the “two-pot system”, which might be effective from 1 March 2024. As a result, people will be able to access their accumulated savings without having to resign from their current employers and incur punitive taxes, which can delay their retirement savings goals. It will also give people an opportunity to invest 1/3 of their pension and provident funds in a savings portion, including retirement annuities, that would have ordinarily been accessible at age 55.

Turning a retirement savings crisis into an opportunity to bolster a savings culture

It is evident that many South Africans are not saving adequately for retirement, given that average replacement ratios are between 25-30%. This is because people pause from saving for retirement throughout their working lives, some are not part of employer-sponsored retirement schemes which act as a “forced saving mechanism” and most people in South Africa don’t have the means to make saving for retirement a priority.

For those who want to bolster their retirement savings, the change in legislation to the two-pot system should be used as a golden opportunity to do so. Here are three starting points to consider:

1. Invest in diversified portfolios that take where you are in life into account

The general rule is, the younger you are when you start to invest, the more risk you should take. If you are getting closer to retirement, however, you should reduce your risk, as you may not have the requisite time to endure major market downturns.

Constructing a portfolio under the two-pot system will still require that you select one that is in line with Regulation 28. Pension and Provident funds will need to have default options for members who cannot choose their own investment portfolios. In the case where you want to kickstart your retirement savings through a retirement annuity, it might be worthwhile to consider multi-asset funds. At PPS Investments, we offer an extensive range of multi-manager and single-managed partnership funds which follow an investment process that offers diversification among underlying managers and has led to competitive performance over the long term, even as market volatility has increased recently.

2. Optimize your savings in the short term by making sound financial decisions, now

Perhaps there might be some of you reading this article, who are changing jobs and may fear that once the two-pot system kicks in, a large portion of your retirement savings will be locked in the 2/3 pot, that vests only at retirement and feel it might be better to withdraw it now before the new legislation comes to effect?

While people have different financial circumstances, it would be worthwhile to transfer the funds, where possible, into a preservation fund, as taxes can be quite high if you choose to withdraw any amount above R27 500. Once the two-pot system is effective, you will be able to make withdrawals from the savings pot, on a rolling basis every 12 months, which will be taxed at your marginal tax rate.

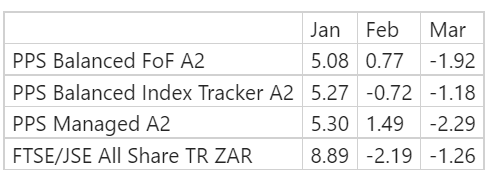

Preserving your investment gives your accumulated savings an opportunity to grow. I know this from my personal experience when I changed jobs recently and preserved my pension fund. This happened in January 2023 and the transfer was finalized the following month, which meant being out of the market for a month. February 2023 was a ‘good’ month in the market as the FTSE/JSE ALSI yielded 8.89% in January 2023. I could have also earned upwards of 5% had I been invested in any of the PPS Multi-Asset High Equity Funds. The diagram below returns to illustrate what I missed out on in January.

While this is a recommended approach, it does not constitute financial advice. Speak to a professional financial adviser who can provide you with a solution that is fit for your purpose.

3. Maximize your time in the market and be mindful of the fees you pay

The key advantage of the two-pot system is that people will have access to making provisions for short-term financial emergencies while staying the course in saving for retirement. The proposed amendments stipulate that any accumulated savings until March 2024 will stay in the vested pot and will be accessible based on the rules of the fund that still apply now.

It makes sense to optimize the growth of that investment by taking advantage of the tax deductions you get when saving through a retirement fund. The government provides a tax-deductible saving of up to 27.5% of your income, which is capped at R350 000 as a rand value before the end of each tax year.

At PPS Investments we provide family members with an opportunity to invest with us, pooling the value of investments to reduce the administration fees they would pay, giving your investments an opportunity to accumulate more growth. The most important thing to do is to stay the course and do time in the market, as investments need a long-term orientation to realise their potential to grow.

About PPS Investments

PPS Investments Group is a subsidiary of Professional Provident Society Insurance Company Limited, a Licensed Insurer, and Financial Services Provider. PPS Investments Group consists of the following authorised Financial Services Providers: PPS Investments (Pty) Ltd(“PPSI”), PPS Multi-Managers (Pty) Ltd(“PPSMM”), and PPS Investment Administrators (Pty) Ltd(“PPSIA”); and includes the following approved Management Company under the Collective Investment Schemes Control Act: PPS Management Company (RF) (Pty) Ltd (“PPS Manco”). Financial services may be provided by representative(s) rendering financial services under supervision. www.pps.co.za/invest

Disclaimer

The information, opinions and any communication from PPS Investments Group, whether written, oral or implied are expressed in good faith and not intended as investment advice, neither does it constitute an offer or solicitation in any manner. Furthermore, all information provided is of a general nature with no regard to the specific investment objectives, financial situation or particular needs of any person. It is recommended that investors first obtain appropriate legal, tax, investment or other professional advice prior to acting upon such information.

{kind=link}